The end of 67 retirement marks a significant shift in the landscape of financial planning and social policy, impacting a generation that has long relied on this age as a benchmark for leaving the workforce. As we delve into the implications of this change, it's crucial to understand the broader context and the specific details that affect individuals and communities alike. This shift is not just a numerical change but a profound alteration in how we perceive and prepare for the later stages of life.

This article aims to provide a comprehensive overview of the end of 67 retirement, exploring its causes, effects, and the strategies needed to adapt. By examining both the personal and societal dimensions of this change, we hope to offer valuable insights for those navigating this transition. Whether you are approaching retirement or planning for the future, understanding the end of 67 retirement is essential in today's evolving economic environment.

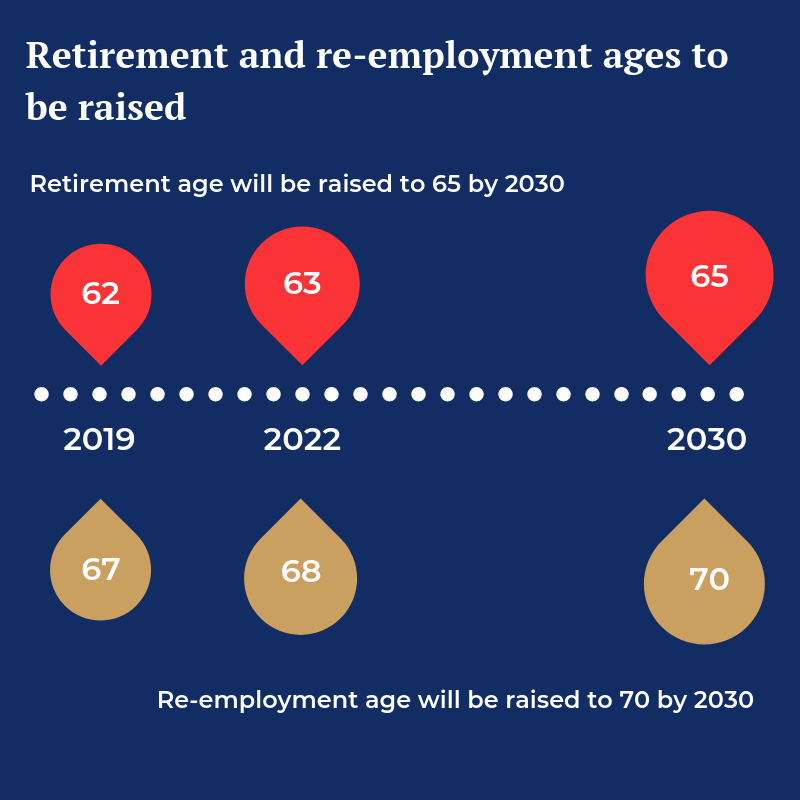

Background on the End of 67 Retirement

The traditional retirement age of 67 has been a cornerstone of retirement planning for decades. However, recent trends and policy changes have begun to challenge this norm. Factors such as increased life expectancy, economic instability, and changes in social security regulations have contributed to a reevaluation of what it means to retire at 67. As individuals and policymakers grapple with these changes, the end of 67 retirement signifies a new era in which flexibility and adaptability are paramount.

Implications for Individuals

For many, the end of 67 retirement means reconsidering their financial strategies and lifestyle choices. Those who had planned to retire at 67 may now need to adjust their savings plans, work longer, or explore alternative sources of income. This shift also presents an opportunity for continued engagement in the workforce, allowing individuals to stay active and contribute to society in meaningful ways. As we explore these implications, it's important to consider the diverse experiences and needs of those affected by this change.

Strategies for Adapting

Adapting to the end of 67 retirement requires a multifaceted approach. Financial experts recommend revisiting retirement savings plans, exploring part-time work opportunities, and considering investments that can provide additional income. Additionally, maintaining a healthy lifestyle and staying engaged in social and community activities can enhance the quality of life during these extended working years. By taking proactive steps, individuals can navigate this transition with confidence and resilience.

Broader Societal Impact

The end of 67 retirement also has broader societal implications. As more people remain in the workforce, businesses may need to adapt by offering flexible work arrangements and creating environments that support older employees. This shift can lead to a more diverse and experienced workforce, bringing unique perspectives and skills to various industries. Policymakers, too, must consider how to support an aging population that remains economically active, ensuring that social security and healthcare systems are prepared to meet evolving needs.

For more information on retirement trends and strategies, consider visiting the AARP Retirement Guide, which offers valuable resources and advice for those planning for their future.

The end of 67 retirement is a complex and multifaceted issue that touches on financial, social, and personal aspects of life. By understanding its implications and taking proactive steps to adapt, individuals and society as a whole can navigate this transition with foresight and resilience. As we continue to redefine what it means to retire, flexibility and adaptability will be key in creating a fulfilling and secure future.